Merchant Accounts: What They Are, How They Work, and How to Choose a Provider

If your business accepts card payments, your bank account is only one piece of the system moving money around. A standard checking account can store funds and send payments, but it doesn’t handle the behind-the-scenes mechanics that make card transactions possible, like authorization, routing, fraud checks, and settlement. That’s where merchant accounts come in.

A merchant account is a specialized account used during the payment process to temporarily hold card funds before they’re deposited into your business bank account. Most businesses that accept credit or debit cards rely on merchant-account infrastructure in some form, whether through a traditional payment processor or an all-in-one platform that bundles those services together.

In this article, we’ll break down how merchant accounts work, how they compare to other payment tools, what kinds of fees businesses can expect, and how to evaluate different providers. We’ll also look at Slash, a business banking platform that helps merchants centralize payment activity and monitor cash flow from a single dashboard.¹

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

What Is a Merchant Account?

A merchant account is a specialized account used to process card payments. When a customer pays with a credit or debit card, the money does not move directly from the customer’s bank account into the business’s checking account. Instead, the transaction passes through a payment-processing system involving the payment processor, the card network, the customer’s issuing bank, the business’s acquiring bank, and the merchant account sitting in the middle.

The merchant account’s job is to temporarily receive and hold card funds while the transaction is processed and settled. Once settlement is complete, the funds are transferred into the business’s operating account, usually within one to three business days.

Merchant accounts exist because card payments involve more coordination and risk than standard bank transfers. Payment processors and acquiring banks use merchant-account infrastructure to manage settlement, fraud screening, chargebacks, and card-network compliance requirements.

Many businesses today do not open a standalone merchant account directly. Payment platforms like Stripe, Square, and PayPal often operate as payment facilitators, or “PayFacs,” allowing businesses to accept payments under a master merchant account maintained by the platform itself. From the business’s perspective, the experience feels simpler, but the same merchant-account infrastructure is still handling the underlying transaction flow.

How Does a Merchant Account Work?

The movement of money from a customer’s card to a business’s bank account happens in several stages behind the scenes. Here’s what that process typically looks like:

- Authorization: A customer taps, inserts, swipes, or enters their card information at checkout. The payment processor sends the transaction through the card network to the customer’s issuing bank, which approves or declines the payment based on available funds, card status, and fraud checks.

- Capture: Once approved, the transaction is captured, meaning the approved amount is reserved against the customer’s account. Some businesses capture transactions immediately, while others batch transactions together later in the day.

- Clearing: The card network facilitates the exchange of transaction information between the issuing bank and the acquiring bank. At this stage, the payment is approved and queued for fund movement, but the money has not yet been deposited.

- Settlement: The issuing bank transfers the funds through the card network to the acquiring bank, minus interchange and network fees. The funds then pass through the merchant account before being deposited into the business’s operating account according to the processor’s settlement schedule.

- Deposit to the business account: After settlement is complete, the business receives the remaining funds in its primary bank account, typically within one to three business days depending on the provider, payment method, risk profile, and banking timelines.

In this process, the merchant account acts as the operational holding layer between the card networks and the business’s bank account. It allows processors and acquiring banks to reconcile transactions, deduct fees, monitor for fraud or chargebacks, and release funds according to the agreed settlement terms.

Merchant Account vs. Business Bank Account vs. Payment Gateway

These terms are closely related, and many modern payment platforms bundle them together, which is why they’re often confused. But each component plays a different role in the payment process. A business bank account stores company funds, a payment gateway securely transmits payment information, and a merchant account handles the processing and settlement of card transactions between the two. Here’s a chart to better explain where each fits in the payment process:

Even after card transactions are processed and settled, your business still needs a bank account where those funds can be deposited and managed. Slash lets businesses receive payouts from Stripe, Shopify, Amazon, and more into the same account you use for operating cash and payments; from there, you can automatically sync transaction data with accounting platforms like QuickBooks Online, Xero, and Sage Intacct to simplify reconciliation and reporting.

Does Your Business Need a Merchant Account?

Most businesses that accept card payments rely on merchant-account infrastructure in some form. The real question is usually whether you need a dedicated merchant account or whether a payment facilitator like Stripe, Square, or PayPal is enough for your business.

A dedicated merchant account may make sense if your business:

- Processes high transaction volume: Larger merchants can often negotiate better pricing and more customized settlement terms directly with processors or acquiring banks.

- Operates a custom checkout or POS system: Businesses with proprietary e-commerce flows or specialized payment infrastructure usually benefit from more direct control over processing.

- Needs more flexibility around payment methods and settlement: Dedicated accounts generally offer more control over payout timing, routing, and supported payment types.

- Operates in a higher-risk industry: Businesses in industries like travel, subscriptions, or high-ticket retail may face stricter controls or transaction limits from payment facilitators.

- Accepts significant in-person payments: Merchants with physical retail operations or complex omnichannel setups often require more tailored payment-processing arrangements.

A payment facilitator may make more sense if your business:

- Is early-stage or processing relatively low volume: Payment facilitators simplify onboarding and reduce operational overhead.

- Wants faster setup: Platforms like Stripe and Square allow businesses to begin accepting payments quickly without establishing a direct acquiring-bank relationship.

- Prefers flat-rate pricing: Simpler pricing structures can be easier to manage for smaller merchants, even if they become less cost-effective at scale.

- Doesn’t want to manage underwriting or compliance directly: The facilitator handles much of the underlying merchant-account infrastructure and risk management on the business’s behalf.

The trade-off is that payment facilitators typically offer less control over pricing, settlement timing, and account policies. Businesses also operate under the facilitator’s broader risk framework, which can affect reserves, payout holds, or account reviews.

What Fees Are Associated with Merchant Accounts?

Understanding the fee categories helps businesses compare providers accurately and model the true cost of card acceptance. Here are some fees you’ll likely encounter:

Transaction and Processing Fees

Transaction fees are charged on each payment processed. They typically combine interchange (the fee paid to the card issuer, set by the card network) with the processor's own markup. Under interchange-plus pricing, these two components are disclosed separately; the merchant sees exactly what the card network charges and what the processor adds. Under flat-rate pricing, they're blended into a single per-transaction rate. Interchange-plus is almost always cheaper for high-traffic businesses, while flat-rate is simpler for lower-volume operations.

Monthly Account and Setup Fees

Many traditional merchant account providers charge monthly account maintenance fees, statement fees, or minimum monthly volume fees. Setup fees for new accounts appear with some providers, but are less common than they once were. These charges add a fixed cost layer on top of variable transaction fees and should be factored into total cost of ownership comparisons.

Payment Gateway and Platform Fees

When a payment gateway is used separately from the merchant account, you may receive a separate monthly gateway fee as well as a per-transaction gateway fee. Some modern bundled platforms roll this into their transaction pricing, but businesses using a standalone gateway alongside an acquiring bank relationship should account for both cost layers.

Chargeback and Penalty Fees

Each time a disputed transaction is reversed by the cardholder's bank, a chargeback fee may be triggered, typically ranging from $20 to $100 per dispute regardless of outcome. Businesses that exceed card network chargeback thresholds (generally around 1% of monthly transactions) may be placed in monitoring programs and face additional fines. These fees aren't always visible in a standard rate comparison, but they can affect the actual cost of processing for businesses in high-dispute categories.

International Payment and Currency Conversion Fees

Businesses accepting electronic payments from international customers often face additional fees, including cross-border assessment fees charged by card networks, currency conversion markups applied by the processor, and different interchange rate schedules for international cards. These can be significant for businesses with consistent international transaction volume.

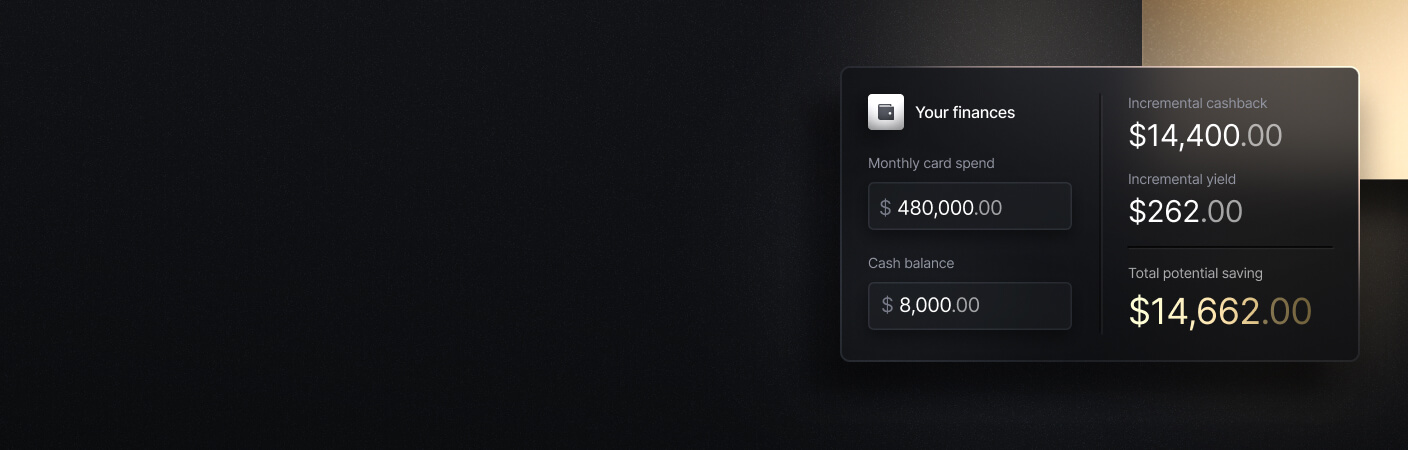

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

How to Choose a Merchant Account Provider

The right merchant account provider can depend on how your business accepts payments, its transaction volume and growth trajectory, and your prioritization of direct control over payment operations. Let’s break this down:

Supported Payment Methods and Integrations

While card payments are the baseline, many businesses need to accept a broader set of payment methods, including ACH bank transfers, digital wallets like Apple Pay and Google Pay, buy-now-pay-later options, and international payment methods. A business expecting to expand internationally or to add payment methods as it grows should confirm that the provider's method coverage and integration ecosystem can scale with their plans.

Settlement Speed and Cash Flow Timing

Standard settlement is typically one to two business days, but providers vary. Some offer same-day or instant deposit options, while others have standard timelines that extend to three or more days for new accounts or higher-risk businesses. For businesses with tight operating cash flow, or those managing payroll or supplier payments against incoming revenue, settlement timing can be a big deal.

Pricing Transparency and Support Quality

A provider with a simple, openly disclosed rate structure is easier to account for than one with a lower stated rate buried under layers of undisclosed fees. It’s smart to request a complete fee schedule, including all fixed and variable components, before signing a contract. Long-term contracts with early termination fees are common in traditional merchant account agreements and warrant careful review.

When a payment holds up, a chargeback arrives, or an integration fails, the speed and quality of provider support determines how quickly the business resolves the problem. Since it’s tough to analyze support responsiveness during the sales process, it can be good to check independent reviews for helpful insights.

Security, Fraud Protection, and Compliance Support

PCI DSS compliance is the security standard for businesses that handle card payment data. However, providers vary in how much compliance support they offer. Some provide self-assessment tools and documentation, while others certify their infrastructure directly, reducing the business's own compliance scope. Fraud detection tooling, chargeback dispute support, and the ability to configure fraud filters are similarly worth evaluating for businesses in categories with higher fraud exposure.

How to Get a Merchant Account

Getting a merchant account usually involves a provider reviewing your business before approving you to accept card payments. Here’s how the process typically works:

- Choose the type of provider: Decide whether you need a dedicated merchant account through a processor or acquiring bank, or whether a payment facilitator like Square, Stripe, or PayPal is enough for your business.

- Gather your business information: Providers usually ask for your legal business name, EIN, business address, ownership details, bank account information, website, and expected processing volume.

- Share your processing profile: Be prepared to explain what you sell, how customers pay, your average transaction size, expected monthly volume, refund policies, and whether you accept payments online, in person, or both.

- Go through underwriting: The provider reviews your industry, transaction model, financial history, time in business, chargeback risk, and, in some cases, the owner’s personal credit history.

- Review pricing and reserve terms: If approved, compare the provider’s processing fees, monthly fees, payout timing, chargeback fees, contract terms, and any reserve requirements.

- Connect your payment tools: Once the account is active, connect your payment gateway, checkout system, POS hardware, e-commerce platform, or invoicing software.

- Start processing and monitor performance: After setup, track settlement timing, fees, chargebacks, refunds, and reconciliation so you can catch issues early.

Higher-risk businesses may face extra scrutiny or higher reserve requirements. This can include industries such as travel, subscriptions, nutraceuticals, firearms, and adult content, where processors may see greater chargeback or fraud exposure. These businesses may need a specialized high-risk processor, which usually comes with higher fees.

Optimize Your Payment Operations with Slash

Understanding how merchant accounts work is only a small part of running your business. As payment volume grows, you’ll need a way to track payouts across different processors, manage your invoices, and move money without relying on disconnected systems.

Slash is a business banking platform that helps businesses manage your money once after it hits your account. Businesses can centralize payouts from platforms like Stripe, Shopify, and Amazon with dedicated merchant services for leading ecommerce marketplaces. Businesses can also collect payments from customers through embedded payment links on invoices created and sent from the Slash dashboard, with support for crypto payments and ACH debiting.⁴

Here are some other Slash features that can simplify how your business moves and manages money:

- Slash Visa® Platinum Card: Issue unlimited virtual and physical cards with customizable spending controls for employee expenses, vendor payments, subscriptions, and more. Eligible purchases can earn up to 2% cash back.

- Multiple payment rails: Send and receive ACH transfers, domestic and international wire payments, RTP/FedNow payments, and supported stablecoin transactions through the same platform.

- AI-powered finance workflows: Twin, Slash’s built-in AI agent, can help businesses review transactions, pay invoices, monitor balances, and answer finance questions through natural-language prompts.

- High-yield treasury management: Earn up to 3.79% annualized yield on eligible idle funds through money market investments managed within the Slash platform.⁶

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

What makes a business “high risk” to a merchant services provider?

A merchant services provider may deem your account "high risk" based on underwriting factors like chargeback exposure, refund rates, and transaction patterns. Certain industries like travel and firearms also carry higher risks in the eyes of providers.

Chargeback Prevention: 6 Ways to Protect Revenue and Reduce Risk

Why might a merchant account provider hold or delay funds?

This may happen to mitigate financial risk, usually triggered by high chargeback rates, suspicious or fraudulent activity, sudden spikes in sales volume, or breaking contract terms.

Is there a difference between credit and debit transactions within a merchant account?

Credit and debit transactions do carry noteworthy differences. Debit transactions (especially PIN-based) are generally cheaper and faster to settle, while credit card transactions offer higher security against fraud but carry higher fees.

ACH Credit vs. ACH Debit: What's the Difference, and How Should Your Business Use Them?

Read more from us