The Hidden Math Behind Credit Card Rewards

The number of credit card ads we see every day can be overwhelming. According to Ad Age, card providers like American Express and Capital One spent more than $4 billion on advertising in 2025. To put that into perspective, that’s three times as much as insurance giant Geico spent on marketing in the same timeframe.

Many of these ads focus on one key feature: rewards. GrowByData, a market intelligence service, conducted a study of card ads in Q1 2025 and found that 9,000 unique ads were created featuring “cash rewards” as a selling point. Those ads promote dozens of different reward structures, from straightforward cash back programs to increasingly complex points ecosystems.

For business owners evaluating corporate cards, the difference matters. While both systems reward spending, they do so in fundamentally different ways. Cash back delivers a fixed return that can be used anywhere, while points programs often promise higher value that depends on how, when, and where those points are redeemed. As a result, the rewards rate printed on a card’s marketing materials rarely tells the full story.

Rewards Rates Tell Half The Story

Cash back rewards are generally the simpler of the two. If a card offers 1.5% flat-rate cash back, you’ll receive 1.5% of your spending back as rewards, typically through statement credits or direct account credits. That’s $15 on $1,000 in spend, $150 on $10,000 in spend, and so on.

Some cash back cards use category-based rewards structures, offering elevated returns on certain types of purchases. A fleet card, for example, may offer higher rewards on fuel purchases than on general spending. Regardless of the structure, however, the value remains easy to calculate. One dollar of cash back is always worth one dollar.

Points-based cards work differently. In a vacuum, many providers value points at roughly one cent each, leading some cardholders to assume that a card earning 2x points is effectively the same as a card offering 2% cash back. This is not the case.

Take the Chase Ink Business Preferred Credit Card as an example. The card offers 3x points on travel, shipping purchases, internet services, and advertising spend. At first, that sounds like a great deal. The challenge is that earning points and redeeming value from those points are two different things.

Unlike cash back, points do not have a fixed value. A point redeemed as a statement credit may be worth one amount, while that same point redeemed through a travel portal or transfer partner may be worth substantially more—or less. Chase points transferred to certain hotel programs can be worth less than one cent each, while airline redemptions may increase their value. The reward earned at the point of purchase never changes, but the value ultimately received does.

That variability is one of the biggest distinctions between points and cash back. Two businesses can spend the exact same amount, earn the exact same number of points, and walk away with completely different levels of value depending on how those rewards are redeemed. With cash back, there is no such gap between what is earned and what is received.

Travel Rewards Are Only Valuable If You Need the Travel

Supporters of points-based rewards programs often point to travel redemptions as their greatest strength. In some cases, they’re right. Certain travel bookings can generate redemption values that exceed the face value of cash back rewards.

The question businesses should ask, however, is whether travel value is actually equivalent to cash value.

Cash can be used for anything: payroll, inventory, software subscriptions, marketing campaigns, or any other business expense. Travel rewards can only be used for travel. A points program may advertise exceptional redemption rates through a preferred airline or hotel partner, but those rates only matter if the available flights, routes, hotels, and booking windows align with your company’s plans.

Consider two companies that each generate $10,000 in rewards over the course of a year. One receives $10,000 in cash back. The other earns points that could potentially be redeemed for $12,000 worth of travel. On paper, the points program appears superior. In practice, that additional value only materializes if the company actually books the travel, uses the recommended redemption channels, and avoids options that dilute the value of its points.

For many businesses, flexibility carries its own value. Travel rewards may offer higher theoretical returns, but cash back provides immediate purchasing power that can be deployed wherever the business needs it most. Finance teams don’t need to evaluate transfer partners, redemption charts, or travel inventories to determine what their rewards are worth. The value is already clear.

Businesses Benefit from Predictability, Not Potential

Points-based cards have earned a loyal following, particularly among frequent travelers. Businesses that spend heavily in bonus categories and consistently redeem rewards through high-value travel channels can sometimes generate impressive returns.

The problem is that most businesses don’t operate on theoretical maximum value. They operate on realized value.

A points card advertising 3x rewards may ultimately outperform a cash back card under ideal circumstances, but reaching that outcome often requires intense attention to detail. Companies must evaluate bonus categories, compare redemption options, monitor changing point valuations, and determine whether travel redemptions actually fit their needs. The more variables involved, the harder it becomes to predict the true return generated by the card.

Cash back rewards remove much of that uncertainty. Every purchase generates a predictable return, allowing finance teams to forecast rewards, measure performance, and incorporate those earnings into broader budgeting decisions without additional calculations.

Time is another consideration. Points enthusiasts often enjoy optimizing rewards programs, researching transfer partners, and searching for the highest-value redemptions. For business owners and finance teams, however, rewards programs are rarely the primary objective. The goal is running the business efficiently. A rewards structure that requires ongoing management may produce higher returns in certain situations, but it also introduces administrative overhead that many organizations would rather avoid.

Ultimately, the strongest rewards program isn’t necessarily the one that promises the highest theoretical value. It’s the one that consistently delivers useful value with the least amount of headache. Businesses shouldn’t have to redesign their spending habits, alter travel plans, or navigate redemption strategies to receive the full benefit of a rewards program. They should be able to spend money on legitimate business expenses, earn rewards, and put those rewards back into the business.

That’s exactly what the Slash Visa® Platinum Card is designed to do.¹

With up to 2% cash back on eligible business spend, the Slash card gives companies a straightforward way to earn rewards without tracking categories, managing transfer partners, or worrying about fluctuating point valuations. Every eligible purchase contributes directly toward cash back that can be reinvested into the business however the company sees fit.

Businesses can also issue unlimited cards to employees, allowing rewards to accumulate automatically across the organization as spending occurs. And to prevent maverick spend, Slash cards come with granular spend controls that can limit employee card usage by setting customizable limits, merchant category restrictions, location settings, and more. Every transaction is logged in your Slash dashboard and automatically categorized for your accounting ledger. And when you want your cashback, all you do is click redeem.

Optimizing business spend is already complicated enough. Your rewards program doesn’t need to be.

Keep it simple with the Slash Visa® Platinum Card.

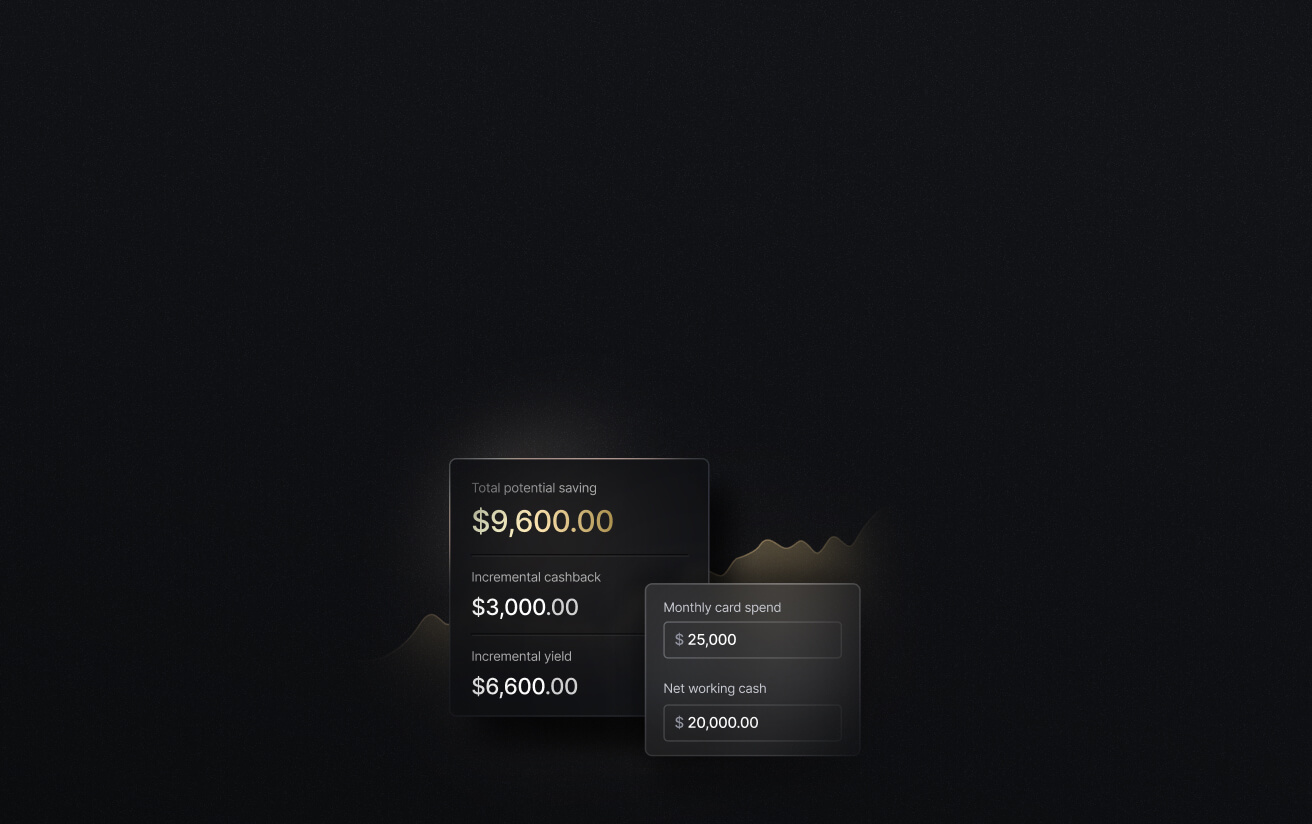

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.