Wholesale Inventory Financing Explained: Types of Funding and Use Cases

Wholesale inventory financing helps product-based businesses pay for inventory before they have the cash on hand to cover it. If you are buying stock in bulk, most suppliers expect payment upfront, while your customers may take time to pay you back. That timing gap can strain your cash flow and make it harder to keep up with demand. Financing gives you access to working capital so you can continue purchasing inventory, fulfilling orders, and growing without putting your operations on hold.

The effectiveness of inventory financing comes down to timing. You are using borrowed capital to purchase stock that will generate future revenue, so repayment depends on how quickly that inventory sells and converts to cash. Whether inventory financing helps or hurts your cash flow depends on how well its terms match your sales and collection cycles, so before applying, it is important to know exactly what you’re getting into.

Slash Capital is a flexible financing option that can be used for your business’s short-term inventory needs.⁵ It provides a line of credit powered by Slope, allowing you to draw funds when you need a quick liquidity boost, with repayment terms of 30, 60, or 90 days. Because it is built into the same platform as your cards, payments, and invoices, you can see how each drawdown affects your cash flow in real time and plan around sales and restocks.¹

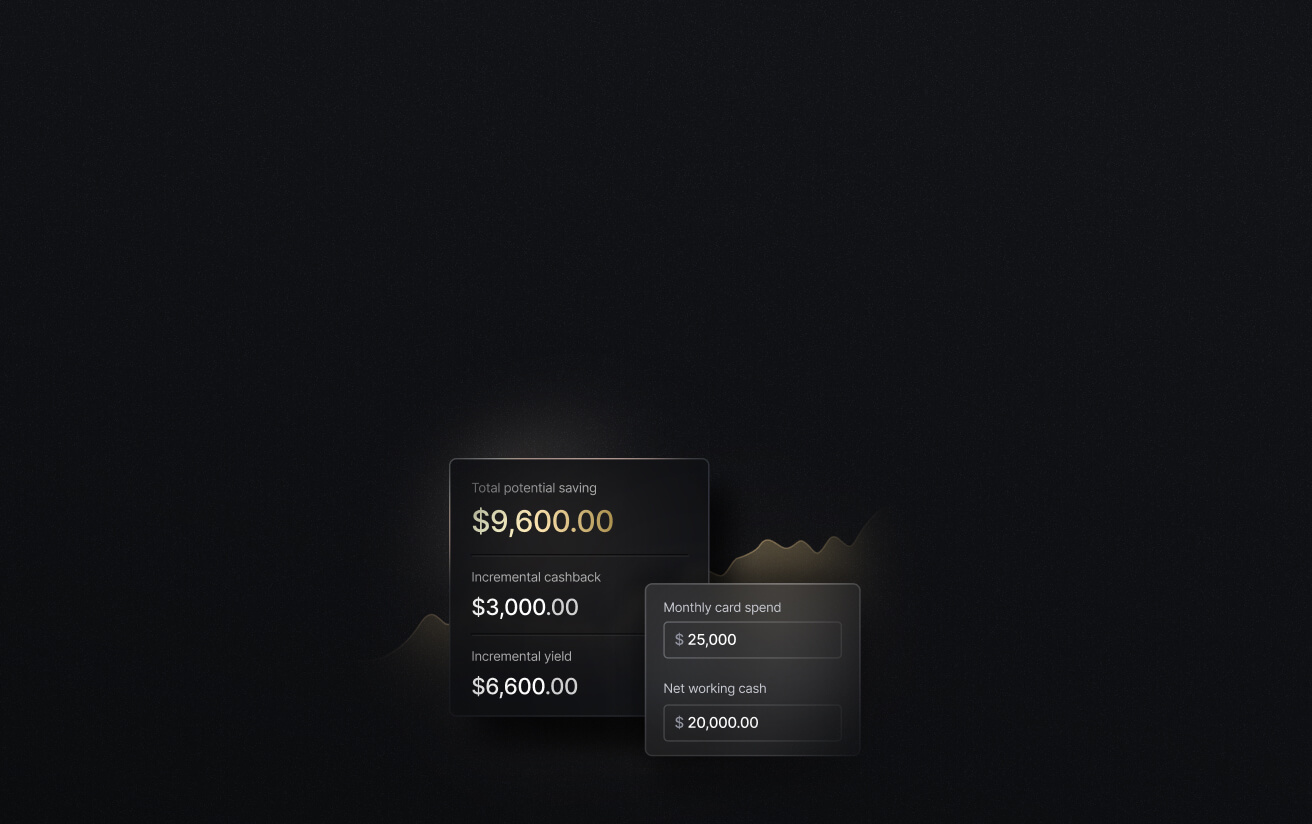

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

What is Inventory Financing?

Inventory financing is a type of business loan or line of credit that allows businesses to borrow against the value of their inventory. In most cases, that inventory serves as collateral, giving the lender some protection if the borrower is unable to repay the loan. Depending on the structure, funds can be used to purchase new inventory or unlock working capital tied up in existing stock.

Wholesale inventory financing is a more specialized version of the same structure. It is intended for businesses that sell goods in bulk to other businesses, such as retailers or distributors, rather than directly to consumers. Wholesalers often receive large purchase orders and need to quickly secure enough inventory to fulfill them, sometimes across multiple customers or product lines.

Instead of financing general inventory levels, wholesale inventory financing is often deployed when order volume increases. That could mean taking on a larger purchase order than usual, supplying a new retail partner, or increasing inventory ahead of a busy season. In these scenarios, financing provides short-term capital so businesses can keep product moving without slowing down other operations.

How Wholesale Distributors Use Inventory Financing

Wholesale distributors often need to spend a large amount of cash upfront to secure inventory from manufacturers or suppliers. As order sizes grow, these purchases become harder to fund with existing cash, credit cards, or occasional short-term loans. Instead, most businesses need a more reliable financing setup that can support ongoing purchases and match longer sales cycles.

Businesses operating in wholesale, distribution, or importing tend to run into a few common challenges:

- High upfront costs when buying inventory in bulk

- Seasonal demand that makes cash flow less predictable

- Payment terms (often 30 to 90 days) that delay when revenue comes in

- For importers, added costs like shipping, customs duties, and taxes

Inventory financing can help smooth out some of the cash flow variability that comes with these challenges. In most cases, financing covers between 50% and 80% of the inventory’s value, depending on the type of goods, how quickly they sell, and how easily they can be resold. It can be structured as a term loan with fixed monthly payments or as a revolving line of credit that you can draw from as needed.

The inventory itself is used as collateral, which reduces risk for the lender. If the loan is not repaid, the lender can recover funds by selling the inventory. In some cases, if the value of that inventory drops or changes significantly, the lender may also place a broader claim on business assets to protect their position.

Different Types of Inventory Financing Options

There are several ways to finance inventory, and each option is designed for a slightly different stage of the purchasing and sales cycle. Some are better for ongoing restocks, while others are tied to specific orders or invoices. Understanding how each one works can help you choose the right structure based on your cash flow, repayment timeline, and overall business needs:

Inventory term loans

An inventory term loan provides a lump sum upfront that is used to purchase inventory. The loan is repaid over a fixed period through scheduled monthly payments, with interest rates set by the lender. This structure works best when you know exactly how much inventory you need to purchase and have a clear timeline for selling it. Because repayment begins immediately, it is important that your inventory turnover aligns with the loan term.

Inventory line of credit

An inventory line of credit gives you ongoing access to capital that you can draw from as needed. Instead of receiving a lump sum, you borrow against a set credit limit and only pay interest on the amount you use. This is a more flexible option for businesses that restock regularly or manage multiple product lines, since you can reuse the credit as you repay it. It is commonly used to smooth out recurring inventory purchases and short-term cash flow gaps.

Purchase order financing

Purchase order financing is used when you receive a large purchase order but do not have the capital to fulfill it. A financing company pays your supplier directly so production or shipment can begin. Once the goods are delivered and the customer pays the invoice, you repay the financing provider, typically with added fees.

Asset-based lending

Asset-based lending allows businesses to borrow against a broader set of assets, which can include inventory, accounts receivable, or equipment. The amount you can borrow depends on the value and quality of those assets. This type of financing is often used by more established businesses that need larger amounts of capital and have multiple asset types to support the loan.

Invoice factoring

Invoice factoring is slightly different from traditional lending. Instead of borrowing money, you sell your outstanding invoices to a third party at a discount in exchange for immediate cash. The factoring company then collects payment directly from your customer. This can improve cash flow if you are waiting on long payment terms, but it comes with fees and may affect how you manage customer relationships.

Trade credit

Trade credit is an agreement with your supplier that allows you to receive inventory now and pay for it later, often within 30 to 90 days. This is one of the most common and accessible forms of inventory financing, especially for established relationships. While it does not involve a traditional lender, it still functions as short-term financing and can help reduce upfront cash outflows. However, it depends on supplier trust and your credit history, and late payments can impact future terms.

Inventory Financing vs. Traditional Business Loans

Inventory financing and traditional business loans both provide access to capital, but they are structured differently and serve different purposes. Inventory financing is tied directly to the value of your stock and is typically used for short-term purchasing needs, while traditional loans are broader and can be used across many areas of the business. Here’s how they compare at a glance:

Slash Capital is not an inventory financing instrument, as it doesn’t rely on your inventory for collateral, but it can still support inventory purchases by providing flexible, short-term access to capital. It gives businesses a way to cover upfront costs and manage cash flow without committing to a more rigid financing structure.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

How to Apply for Wholesale Inventory Financing

Applying for inventory financing is more involved than a standard loan application. You’ll need to define your inventory needs and provide supporting business and inventory details as part of the process. Here’s a general breakdown of the application and approval process:

Step 1: Define what you need financing for

Start by identifying why you need the financing and how much capital you are trying to access. Having a clear use for the funds makes it easier to compare financing options and explain your request during the application process.

Step 2: Gather your business and financial documents

Most lenders will ask for basic business and financial information before reviewing an application. That often includes:

- Formation documents

- Recent bank statements

- Profit and loss statements

- Balance sheets

- Tax returns

- Any details on existing debt

Some lenders may also want inventory reports, accounts receivable aging, or projections showing how the financing will be repaid.

Step 3: Provide details about your inventory

Because your inventory is your collateral, lenders will want to understand what you sell, how fast it turns over, and how easy it would be to liquidate if needed. They may review the type of inventory, its condition, turnover rate, concentration risk, and whether its value is stable or likely to depreciate quickly. This information helps determine how much you can borrow relative to your inventory’s value.

Step 4: Go through underwriting and collateral review

Even though this is asset-based financing, lenders still review the overall health of your business. They are trying to understand whether you can manage repayment alongside your existing obligations. This usually involves a review of your cash flow, current liabilities, and payment history. In some cases, lenders may also place a lien on your inventory or require ongoing reporting as part of the agreement.

Step 5: Review the financing structure and terms

If your application moves forward, the lender will present the financing terms. This is where you will see how the loan is structured and what repayment will look like. Pay attention to:

- Repayment schedule and monthly payments

- Interest rates and fees

- Any additional collateral requirements or personal guarantees

- Restrictions on additional borrowing

Step 6: Receive funds and manage ongoing reporting

Once finalized, funds may be disbursed as a lump sum or made available through a borrowing line, depending on the structure. From there, your business will need to keep up with repayment and any ongoing lender requirements, such as updated inventory reports, borrowing base certificates, or financial statements. In asset-based lending, the amount available may change over time based on changes in value of the eligible collateral.

How Slash Can Help You Manage Inventory Costs

Slash Capital gives businesses a flexible way to access working capital when they need it. While it is not an inventory financing product, it can be used to fund inventory purchases, cover supplier payments, or bridge short-term cash flow gaps. Instead of committing to a fixed loan, you can draw from a line of credit as needed and repay on a timeline that aligns with how your inventory sells and your customers pay.

Beyond financing, Slash is a full business banking platform designed to support how you manage your finances. You can handle payments, issue cards, send invoices, and track cash flow from a single dashboard, with real-time visibility into your financial position. By keeping your banking, spending, and financing in one place, it becomes easier to stay organized and make decisions during your busiest sales season. Here are some additional features that can support your wholesale operations:

- Slash Visa® Platinum Card: A corporate charge card that earns up to 2% cash back on company spending, with configurable spending rules, card controls, and encryption-grade fraud protection.

- Accounting & ERP integrations: Sync transaction data with QuickBooks Online, Xero, or Sage Intacct to streamline reconciliation, reporting, and month-end close.

- Diverse payment methods: Slash supports a wide range of payments, including card spend, global ACH, international wire transfers to over 180 countries via SWIFT, and real-time domestic payments through RTP and FedNow.

- AI-powered financial tools: Use Twin, our built-in AI agent, to manage your Slash dashboard. You can ask it to create cards, pay invoices, review your cash flow, and much more.

- Invoice management: Create professional invoices using saved client details and collect payments through embedded links supporting ACH, wires, or cryptocurrency.⁴

- High-yield treasury: Earn up to 3.83% annualized yield on idle funds with money market investments from BlackRock and Morgan Stanley, managed directly within your Slash account.⁶

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently asked questions

What types of inventory qualify for financing?

Most lenders prefer inventory that is easy to resell and holds its value, such as finished goods with consistent demand. Perishable items, highly customized products, or inventory that depreciates quickly are less likely to qualify or may receive lower financing amounts.

How to Get a Working Capital Loan: Key Insights for Small Business Owners

What happens if inventory doesn’t sell as expected?

You are still responsible for repayment based on the agreed terms, even if sales are slower than expected. If issues come up, some lenders may be willing to work with you, but in cases of non-payment, they can recover funds by selling the inventory used as collateral.

Working Capital Management: Strategies for Business Growth