Ramp vs Mercury: A Comparison of Banking and Spend Management Solutions

At first glance, Mercury and Ramp may appear similar. They’re both digital-first financial platforms built to modernize business banking. They feature intuitive interfaces, comparable toolsets, and a shared goal of making financial management simpler and more efficient. However, these platforms have more differences than meets the eye.

Although Mercury and Ramp continue to expand their platforms, they each approach financial operations through their own lens. For example, Mercury offers more credit products than Ramp, while Ramp surpasses Mercury in integration capabilities.

Before you decide which option fits your business’s needs the most closely, you should understand how they differ. In this guide, we’ll compare the key features and products across all three and discuss the ways modern teams can take advantage of each. We’ll also highlight the comprehensive financial infrastructure, industry-leading rewards, cryptocurrency support, and capabilities that set Slash apart.¹,⁴ Slash is a business banking platform that combines the banking, payments, and operational tools that exist across both competitors into a single system. That means you’ll only need one login to access your checking accounts, working capital, accounting systems, treasury, and much more.⁵,⁶

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

What You Need to Know About Mercury and Ramp

Both of these platforms champion a digital-first approach focused on streamlined tools, automation, and greater versatility. While they have quite a few tools in common, other aspects of their offerings vary widely, from the types of businesses they serve to the services they deliver. Here’s a brief look at what sets them apart:

What is Mercury?

Mercury launched in 2019 as a banking platform built for startups. Today, Mercury serves late-stage startups, tech companies, and mid-to-large organizations looking for software-driven financial operations.

Here’s a quick look at what Mercury offers:

- $0 fees on checking, savings, and USD wires: Mercury charges no monthly maintenance fee, no minimums, and $0 on domestic and international USD wire transfers, which can add up to meaningful savings for high-transaction businesses.

- Treasury yield: Mercury Treasury offers up to 3.61% annualized yield, managed through J.P. Morgan Asset Management and Morgan Stanley. It’s not a bad yield, but it comes in at a lower rate than Ramp and Slash.

- Enhanced FDIC coverage: Deposits are insured up to $5M through Mercury's partner bank sweep networks, well above the standard $250K limit at traditional banks.

- Accounting integrations: Syncs with QuickBooks, Xero, and NetSuite, with AI-powered transaction categorization and automated bill pay.

- Limited card rewards: Mercury's credit cards earn a flat 1.5% cash back, which trails competitors like Slash that can earn up to 2%.

- Foreign transaction fees and payment rails: Mercury applies a 3% foreign transaction fee and does not support RTP or FedNow for real-time domestic payments. In 2024, Mercury also drew criticism after closing accounts across Africa with limited warning to affected customers.

What is Ramp?

Ramp began in 2019 as a corporate card and spend-management platform focused on automation. It partners with Celtic Bank, Column N.A., Intrafi Network LLC, and others for its banking and credit products. Ramp is built for high-growth startups and SMBs looking for an automation-heavy corporate card program or access to a large number of third-party integrations.

Here’s a look at what Ramp comes with:

- Automation tools: Ramp supports AI-powered receipt matching, automated expense categorization, and smart approval workflows that keep finance teams out of the manual review loop.

- Global reach: Cards are issued in 30+ countries and accepted in 200+ countries on the Visa network, with reimbursements available in 60+ countries across 40 currencies.

- No personal credit checks or personal guarantees: Credit limits are based on business financials like revenue or capital raised, with no impact to personal credit scores.

- Limited card rewards: Like Mercury, Ramp offers flat 1.5% cash back on card spend.

- Treasury yield: Ramp’s treasury yield essentially comes from its expert-managed investment portfolio within their Treasury suite. As of July 2026, this rate comes in at 4.15%.

- No native cryptocurrency support or flexible financing: Ramp doesn't support stablecoin wallets, crypto payouts, or on/off-ramp functionality for cross-border payments. It also doesn't offer tailored lines of credit or other working capital financing products that a platform like Slash comes with.

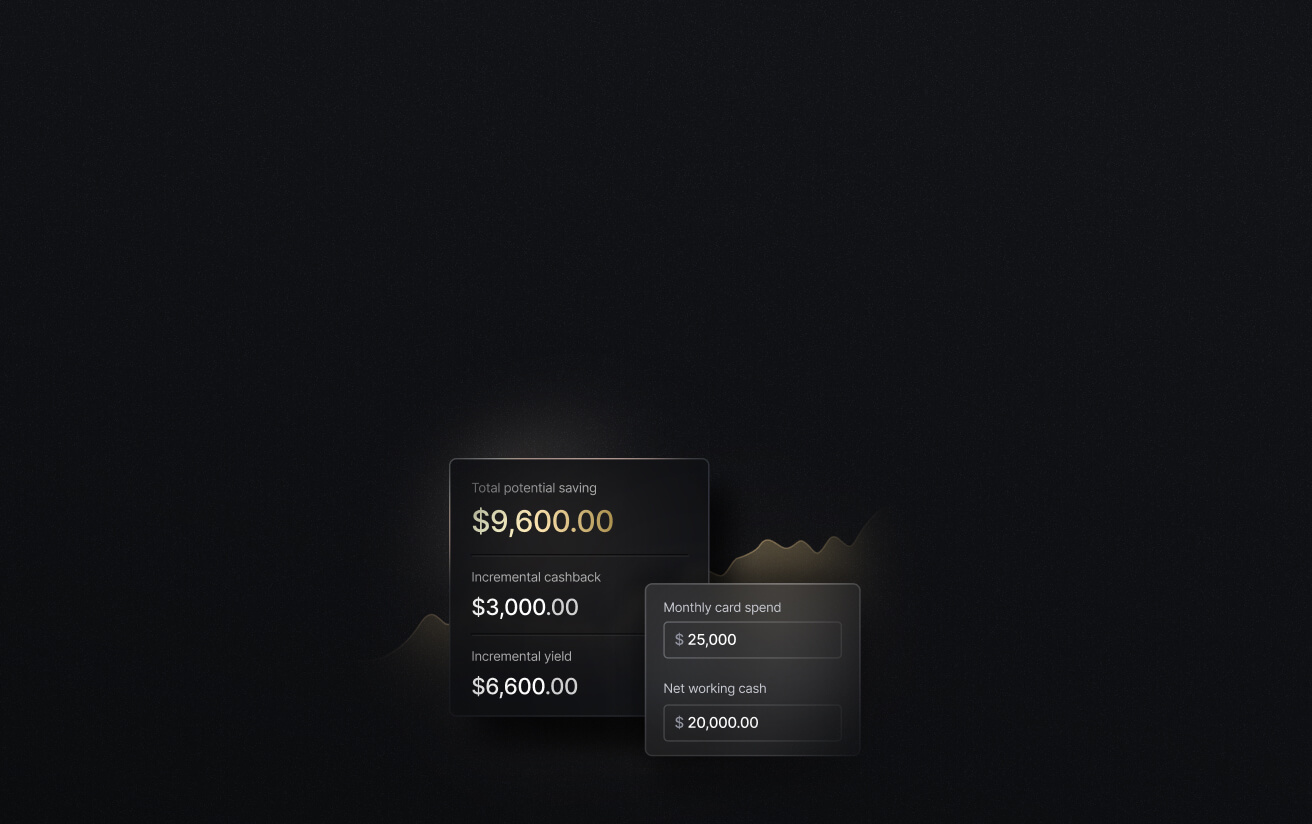

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

How do Mercury and Ramp Compare?

To understand how each platform stacks up, let’s look at a breakdown of how Mercury and Ramp compare across their key products and features:

Typical qualifications and ease of account setup

Fintech platforms tend to offer more obtainable qualification requirements than traditional banks. They often rely less on credit checks, personal guarantees, and extensive financial documentation. That said, Mercury is a little easier to apply for than Ramp. With Ramp, you’ll need at least $25,000 in a U.S. business bank account to qualify, and underwriting is based primarily on your company’s revenue or cash reserves. You don’t need a certain checking balance for Mercury unless you’re applying for their credit card product, which requires various minimums.

Corporate card features

Both platforms offer corporate cards designed to sync transaction data directly into their systems, which can simplify expense management, cash flow visibility, and accounting integration. Ramp issues corporate charge cards, which require full repayment each billing cycle and do not extend revolving balances. Mercury calls their IO card a business credit card, but it’s actually a cash-underwritten charge card, which means the balance you hold on the card can’t exceed the cash you have in Mercury. They both offer up to 1.5% cash back, which comes in below an alternative like Slash that comes with up to 2% cash back on card expenses.

Treasury and high-interest account features

Mercury and Ramp’s treasury features can both offer users solid returns on idle cash, but they work slightly differently. Mercury’s treasury account offers 3.61% annualized yield through J.P. Morgan and Morgan Stanley backing, which is a relatively traditional setup. Within Ramp’s treasury suite is an “Investment Account” that earns up to 4.23% yield. It’s professionally managed and auto-balanced, which is a touch different from other treasury products, but it works more or less the same way from the consumer’s point of view.

Accounting software integrations

Ramp has a leg up on Mercury when it comes to accounting integrations. Ramp connects to 30+ ERPs and accounting systems, including QuickBooks, Sage Intacct, NetSuite, Zoho Books, Trimble Vista, and more. Meanwhile, Mercury only offers integrations with QuickBooks, Xero, and NetSuite.

Insured Cash Sweep (ICS) programs

ICS programs increase FDIC coverage by distributing deposits across a network of partner banks. While FDIC insurance normally tops out at $250,000 per account, these sweep networks can extend protection into the millions (depending on the platform and the business’s total balance). Fortunately, Mercury and Ramp both offer expanded FDIC protection through their respective partner-bank networks.

Bill pay and payment processing capabilities

Ramp’s bill pay feature includes AI-powered invoice capture, multi-level approval workflows, and a full procure-to-pay workflow that integrates deeply with accounting softwares. Overall, it’s built around AP automation, which makes it better suited for finance teams that process significant vendor invoice volume. Mercury, by contrast, frames payments as a banking feature rather than an AP product. They support bill pay, domestic and international wires, ACH transfers, and invoicing, but the workflow depth and approval automation tend to be lighter than what Ramp offers.

Additional Alternatives to Ramp and Mercury

These two platforms aren’t the only ones in the financial services hemisphere. You’ll often run into several other solutions as you evaluate different business banking systems. Below is a quick look at some additional competitors in the space:

- Brex: Brex is another fintech platform that specializes in automation, data organization, and software integrations. Rather than straightforward cash back rewards, Brex’s corporate card uses a points-based system geared toward tech-forward and high-growth companies. Points can provide similar returns to flat cash back, but managing it all can be a headache. In April 2026, Brex was officially acquired by Capital One.

- American Express: Amex is known for its reliability and premium rewards through its Membership Rewards program. It offers a wide range of credit and charge cards, each with different point structures, introductory offers, qualification requirements, and annual fees. While it offers quite a few strong cards, Amex lacks the automation capacity and expense-management tools that modern fintech platforms provide.

- Bluevine: Bluevine is a business banking platform that comes with strong lending capabilities. They offer credit lines of up to $250,000, and users can access their funds within two business days of application. However, they lack the automated expense categorization that’s common among other fintech platforms. Additionally, users can only make international wire transfers to 32 countries, while solutions like Slash unlock access to 180+ countries through several different payment methods.

- Stripe: Stripe is a global financial technology company that provides software and application programming interfaces (APIs) for businesses to accept payments, manage subscriptions, and run their financial operations online. Stripe also offers business banking and financial management services primarily through Stripe Treasury and partner integrations like Stripe Atlas.

Making the Right Financial Move With Slash

Many financial platforms can help streamline money management, reduce manual work, and improve overall efficiency. The problem is that few offer the kind of all-in-one experience that growing businesses actually need to stay competitive. Slash brings banking, payments, crypto tools, and rewards together in a single platform that feels cohesive and easy to use.

Slash also offers a wider range of capabilities that support both day-to-day tasks and long-term planning. You can move money through diverse payment rails, earn strong cash back on purchases, and grow idle funds through high-yield treasury options. Everything works together so you can manage more of your financial workflow in one place with less friction.

Some of Slash’s key features include:

- Built-in cryptocurrency support: Slash lets you on- and off-ramp USD-pegged stablecoins like USDC and USDT. This can give you access to near-instant global transfers that avoid traditional processing delays and interchange fees.

- Agentic AI: Slash comes with Twin, a built-in AI agent that can be prompted with natural language to complete complex tasks. Users can ask it to create cards, pay invoices, review your cash flow, and much more.

- Slash Working Capital: Our financing solution allows you to draw funds directly from the dashboard with flexible 30, 60, and 90-day repayment terms, which can provide short-term liquidity that supports faster scaling.

- Competitive treasury yield: At 3.82%, Slash’s treasury yield settles in between Ramp and Mercury.

- Industry-leading cash back: Mercury and Ramp’s corporate cards earn up to 1.5% cash back, while the Slash Visa® Platinum Card can earn up to 2%.

- Dynamic transfer options: Beyond standard ACH and wire transfers, Slash natively supports real-time payments via RTP and FedNow, plus USD-denominated stablecoin transfers across eight major blockchains.

The future of business finance is simpler, faster, and more connected. Make the shift with Slash and stay ahead of whatever comes next.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

Which platform is more suitable for early stage startups vs established businesses?

While Mercury, Ramp, and Slash offer compatibility with early stage companies, Slash may be the most accessible. Slash has a streamlined application that requires an EIN, articles of incorporation, and evidence of recent banking activity. For our specialized Global USD Account, qualifying is even more straightforward, as you don’t need to have a U.S.-registered LLC.³

How to Start a Startup: How to Get from Idea to Series A Funding

Which platform is more suitable for e-commerce and tech businesses?

Slash is a vertical-specific business banking platform with tools tailored for e-commerce and tech. E-commerce companies can benefit from Slash’s multi-entity support to manage accounts for multiple storefronts, and you can make fast, cheap vendor payments with USD-pegged stablecoins. Tech companies get powerful employee spend management with Slash Cards, detailed cash flow insights, and the configurable Slash API.

A Guide for E-Commerce Bookkeeping: Streamline Your Online Business Finances

How do the corporate card rewards compare across Ramp, Mercury, and Slash?

Slash leads on rewards, offering up to 2% cash back on the Slash Visa® Platinum Card, while both Ramp and Mercury cap out at 1.5% cash back. All three issue corporate charge cards designed to streamline expense management. Notably, Mercury’s IO card is cash-underwritten (your card balance can’t exceed your Mercury cash), whereas Ramp and Slash issue standard charge cards that require full repayment each cycle.