What is USDC, and How do USDC Payments Work?

The infrastructure underlying money movement has gone through quite a few changes. The invention of wire transfers, ACH, and real-time payment rails like FedNow have each compressed settlement times and expanded what businesses could do. Stablecoins represent the next step in that evolution: a digital dollar that moves like an email, settles in minutes, and operates without the geographic and operational constraints of the traditional banking system. One of the most commonly used stablecoins is USDC (USD Coin).

For financial managers and business owners navigating global commerce, understanding how USDC works and where it fits alongside traditional payment methods is important. Companies that adopted ACH early saved on wire fees. Businesses that adopt USDC early gain an edge in cross-border speed, cost, and programmability that their slower-moving competitors simply can't match.

This guide explains the mechanics, the benefits, the risks, and where the technology fits in a modern business treasury stack. Stablecoins like USDC are natively supported by Slash, a business banking platform that enables seamless blockchain payments alongside the rest of your financial stack.¹, ⁴ Slash users can securely hold USDC and easily convert it to cash with built in crypto on/off ramps, saving time, capital, and stress.

Crypto Glossary

Here’s a quick glossary to get you up to speed on some important terms before we break everything down:

- Cryptocurrency: A form of digital currency that can be used for both electronic payments and as a store of value. Cryptocurrencies use cryptography to secure transactions and record them on a public ledger.

- Stablecoins: Virtual tokens designed to maintain price stability, usually by being linked to an underlying fiat currency. The two most popular stablecoins in use today are USDC and USDT, which are both pegged 1:1 to the U.S. dollar.

- Fiat currency: Federally-issued money that is declared legal tender, such as the U.S. dollar or the EU’s euro. The value of fiat currencies comes from their issuing government and central bank instead of a physical commodity like gold.

- Blockchain: A decentralized ledger that records and verifies transactions across a network of computers rather than relying on a centralized authority. Once a transaction is confirmed and added to the blockchain, it becomes very difficult to alter. This structure allows payments to be verified and settled without relying on an intermediary like a correspondent bank.

- Decentralization: The transfer of control and decision-making from a centralized entity (like a bank or government) to a distributed network of participants. Decentralization ensures no single entity controls the blockchain, enhancing censorship resistance, security, and trustless operation.

- Smart contracts: Self-executing contracts that automatically enforce agreements when predetermined conditions are met, such as terms agreed upon by buyers and sellers. This means human intervention and third-party verification aren’t required.

- Custody services: The secure storage and management of digital assets on behalf of a customer. A custodial service holds a user’s private keys and controls their funds, while a non-custodial service gives the user full control.

- Decentralized Finance (DeFi): A blockchain-based financial system that removes intermediaries like banks and brokers, allowing users to lend, borrow, trade, and earn interest directly via smart contracts.

What Is USDC (USD Coin)?

USDC is a stablecoin whose value is pegged 1:1 to the US dollar. Unlike Bitcoin or Ethereum, whose prices fluctuate with market sentiment, one USDC is always worth one US dollar. That stability is what makes it useful as an actual payment instrument rather than a speculative asset.

USDC was launched in September 2018 by Circle, a financial technology company, initially developed through a partnership with Coinbase under the Centre Consortium. Today, Circle operates as the sole issuer. The way backing works is straightforward: every USDC token in circulation is backed by an equivalent reserve of US dollar assets. Circle publishes monthly attestation reports prepared by independent accounting firms, providing verifiable evidence that their reserves closely match circulation.

An important advantage to USDC (as well as all stablecoins) is its speed. USDC transactions settle in minutes, around the clock, every day of the year. There's no concept of "banking hours," no cutoff time for same-day processing, and no distinction between a Monday and a Saturday. For a business collecting payments from international customers, this means working capital arrives immediately instead of sitting in a clearing system for days.

As of 2025, USDC has achieved broad institutional adoption, with companies including Sony, Shopify, and Stripe accepting USDC payments in various capacities. Its market capitalization places it among the largest stablecoins globally, with tens of billions in circulation at any given time.

USDC vs USDT

The main stablecoin alternative to USDC is USDT (USD Tether), which is the largest stablecoin by market cap and the oldest major player. USDT is also pegged 1:1 to the U.S. dollar, and essentially functions in the same way. However, Tether has faced persistent criticism over the opacity of its reserve backing, which can be a concern for businesses that want confidence that their funds are fully covered. Multiple regulatory settlements and ongoing scrutiny have kept USDT at arm's length for many institutional users, despite its liquidity dominance on trading platforms.

Another difference between the two is the fact that USDC is compliant with the European Union’s Markets in Crypto-Assets (MiCA) regulations, while USDT is not. The MiCA regulation is the EU’s legal framework that enforces uniform rules for crypto-asset issuers and service providers (CASPs) across the EU. This means that Circle’s token tends to be used more in Europe.

USDT vs USDC: Making the Right Choice for Stability and Liquidity

How USDC Payments Work: Step-by-Step Process

Understanding the mechanics behind stablecoins can make the adoption of USDC less daunting. Here's how a USDC payment moves from sender to recipient:

Wallet setup and verification

Before using USDC, you’ll need a digital wallet that can store, receive, and send tokens. You may choose to open a custodial wallet, where a third party manages your private keys, or a non-custodial wallet that allows you to be in charge of your own keys. Custodial wallets can also offer insurance coverage for theft and misuse of funds, so they may be preferred by businesses who value security. However, these wallets often come with more fees than non-custodial wallets, as they incur intermediary service costs.

Creating a payment request

When requesting payment in USDC, the recipient generates a wallet address, which consists of a long string of characters that identifies where funds should be sent. In contrast to private keys, which are like banking passwords, digital wallet addresses are public keys that work similarly to bank account numbers.

This payment request specifies three elements: the wallet address where USDC should be sent, the amount requested, and which blockchain network to use. USDC is most commonly traded through Ethereum (ERC-20), but can be sent through over a dozen networks in total. Slash supports eight blockchains, including Tron, Ethereum, Solana, and more.

Transaction initiation

The sender enters the recipient's wallet address and the amount of USDC to send, then authorizes the transaction. This can also be triggered programmatically via smart contract or API, which can be a key advantage for businesses automating payments.

Crypto transactions often carry small charges called gas fees, which can vary based on network demand. On a network like Tron, transactions typically range from $0.30 to $2. Heavy traffic on Ethereum used to spike fees up to $25, but nowadays these charges rarely surpass $1. While some blockchain wallets carry their own transfer charges on top of gas fees, Slash's banking platform does not. With Slash, users can send and receive stablecoins with the same speed and cost that an exchange offers.

Blockchain confirmation and settlement

The transaction is broadcast to the blockchain network, validated by nodes, and included in a block. Depending on the network, confirmation typically takes seconds to a few minutes. Once confirmed, the transaction is final and immutable.

If you want to check the status of a transfer initiation, you can search for your unique transaction ID on blockchain databases. Given how quickly payments are confirmed on a blockchain, you’ll know something has gone awry if a transfer is pending for more than around 10 minutes.

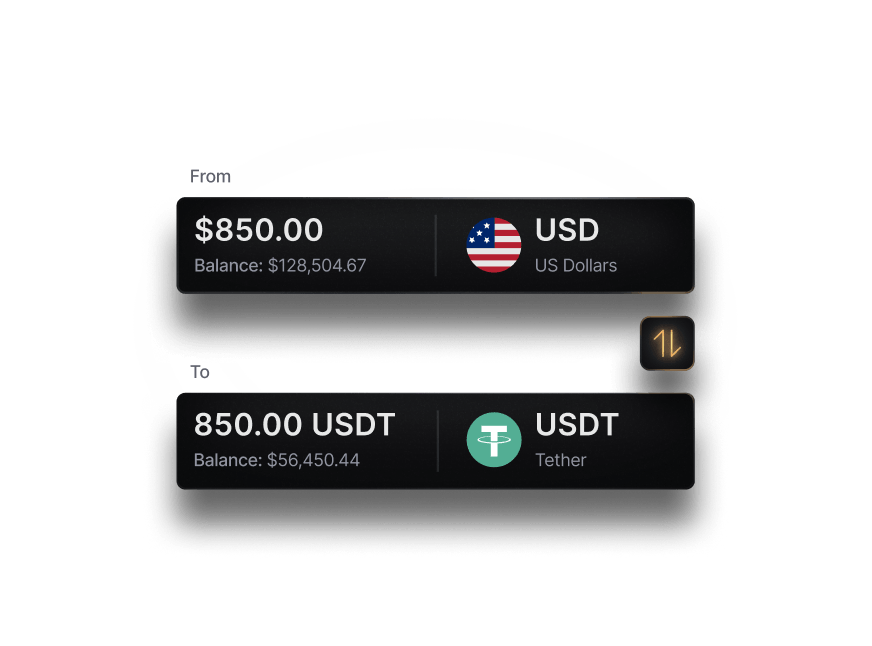

Conversion back to fiat (if needed)

If the recipient wants US dollars rather than USDC, they can convert instantly through an on/off ramp, which is a function that exchanges USDC for USD and deposits it to a bank account. At Slash, we built this tool directly into our platform, allowing businesses to move between USDC and fiat without leaving their banking interface.

Slash business banking

Works with cards, crypto, plus cards, crypto, accounting, and more.

Benefits and Risks of USDC Payments

While there are plenty of advantages to using stablecoins like USDT, you may also encounter some unique risks. Here’s a quick overview:

Key Benefits for Businesses

- Reduced transaction fees: International wire transfers typically cost $25–$50 per transaction, and correspondent bank fees can reduce the amount received. USDC transfer fees depend on the blockchain but can be under $1 on some networks, such as Polygon or Solana.

- Faster settlement: Stablecoins settle in minutes, while traditional rails can take days. The operational implications are significant: better cash flow visibility, reduced working capital tied up in transit, and the ability to move money at any time without being tied to bank processing windows.

- Global accessibility: USDC enables digital wallet transfers across a wide range of geographies, without the need for correspondent banking relationships or foreign exchange spread on USD-to-USD transfers.

- Immutable transaction records: Every USDC transaction is permanently recorded on a public blockchain. This creates an auditable, tamper-proof trail that can simplify reconciliation and support compliance documentation.

- Programmable payments: Smart contracts enable payment logic that doesn't exist in traditional banking. Automatic disbursements, conditional releases, recurring payments, and multi-party settlement structures are all possible with digital tokens.

Potential Risks and Considerations

- Regulatory uncertainty: While Circle operates in a well-regulated manner, the broader stablecoin regulatory environment remains in flux in some jurisdictions. Businesses operating internationally should monitor developments and ensure their use of USDC aligns with local requirements.

- Smart contract risk: Code vulnerabilities can sometimes be exploited. While USDC's core contracts are heavily audited, any application built on top of them carries its own risk profile. Businesses should use well-established platforms rather than novel DeFi protocols for commercial payments.

- Counterparty risk with reserves: USDC is only as stable as Circle's reserve management. While Circle publishes attestations and is regulated, an unexpected reserve failure could affect the peg. Businesses holding large USDC balances should treat this as they would any institutional counterparty risk.

- Wallet security: Unlike a bank account, a self-custodied crypto wallet has no recourse mechanism if private keys are lost or stolen. For most businesses, using a custodial solution can substantially mitigate this risk.

- Merchant acceptance: USDC acceptance is growing rapidly, but it’s not universal. Since businesses can't yet pay most suppliers or vendors in USDC, the on/off ramp transition to fiat remains a necessary bridge in many situations.

Common Use Cases for USDC Payments

USDC's characteristics can be helpful in a variety of business scenarios where standard payment methods aren’t fast or cheap enough:

International supplier payments

Paying overseas manufacturers or vendors via wire is often slow and expensive. A $50,000 payment to a supplier in Taiwan might cost $40–$60 in fees, take three business days to arrive, and show up short due to correspondent bank deductions along the way. USDC settles in minutes with negligible fees, meaning the recipient gets exactly what was sent exactly when they want it. This can also be useful for freelancers and contractors in markets where traditional banking infrastructure is limited or cumbersome.

Cross-border e-commerce

Merchants selling internationally can accept USDC and receive payment immediately without the currency conversion friction of credit card networks. They also won’t have to worry about chargebacks, as blockchain transactions are final and irreversible. USDC is particularly helpful for high-value transactions where credit card processing fees represent a meaningful margin impact.

B2B marketplace transactions

Multi-party marketplaces can use USDC's programmable features to automate settlement by splitting payments between platform, seller, and logistics partners in a single transaction. Thanks to smart contracts, no manual disbursement process is required.

Remittances and international money transfers

For businesses sending regular payments to individuals or small vendors in emerging markets, USDC can offer dramatically better economics than traditional remittance services, many of which charge 5–8% for international transfers. Stablecoins can also beat even the quickest settlement times that remittance services can offer.

USDC vs Other Payment Methods: Comparison

Let’s look at a breakdown that compares USDC with two of the most popular traditional payment rails, wire transfer and ACH:

*Chain gas fee only; platform or processor fees may apply (typically 0.5%-1%)

Ultimately, USDC isn't a replacement for every payment method. ACH still makes sense for domestic vendor payments where speed isn't critical, and wire transfers remain the fallback for recipients who don't yet accept USDC. For international transactions, high-volume supplier payments, or any scenario where speed and cost matter, USDC can offer a structurally superior alternative.

Explore Global Payment Infrastructure With Slash

While USDC can enable fast global transfers, companies still need structured systems to track payments, reconcile transactions, and introduce crypto to their accounting workflows. The Slash business banking platform is purpose-built for both fiat currency transfers and blockchain-powered stablecoin transactions.

Our platform supports dedicated on/off ramps for both USDC and USDT, allowing businesses to convert their cryptocurrency of choice into fiat currency with fees of less than 1% per transaction (minimum $0.40). We also offer our own USD pegged stablecoin, USDSL, which is backed by U.S. Treasury bills and USDC.³ Eligible Slash users have access to a custodial wallet that isn’t connected to an exchange and can be used for payments and native cash conversion.

As companies exchange stablecoin payments with their vendors and partners, all transactions are visible and trackable alongside each other in real time on the Slash dashboard. Wire transfers, employee card spend, incoming/outgoing invoices, and USDC payments are all managed in the same spot. We serve as the financial operations layer that helps teams manage crypto and fiat payments together in a unified workflow.

Other helpful Slash features include:

- AI-powered finance: Our platform comes with Twin, a built-in AI agent that can be prompted with natural language to complete complex tasks. Users can ask it to create cards, pay invoices, review your cash flow, and much more.

- Slash Visa® Platinum Card: The Slash Card allows you to set customizable spending controls and issue unlimited virtual cards for handling team expenses, vendor payments, subscriptions, and more. Users can also earn up to 2% cash back on business purchases.

- Accounting & ERP integrations: Sync transaction data with QuickBooks Online, Xero, or Sage Intacct to streamline reconciliation, reporting, and month-end close.

- Working capital financing: Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to help bridge cash flow gaps.⁵

Stablecoins like USDC offer tangible advantages over traditional payment rails, especially when it comes to speed and price. If your business is ready to connect cryptocurrency with its current financial stack, the Slash platform is here to tie it all together.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently Asked Questions

Can a stablecoin ever become de-pegged from fiat currency?

It's possible, but rare. In March 2023, for instance, USDC became temporarily de-pegged from the U.S. dollar when Silicon Valley Bank collapsed. Outside of unexpected events like that, stablecoins should stay linked 1:1.

What is a Stablecoin? Definition, Types, and How it Works

What are crypto debit cards?

Crypto debit cards are specialized debit cards, sometimes offered by crypto exchanges, that link to your digital wallet. These cards can be used to buy goods priced with fiat currency, with the equivalent amount of stablecoin deducted from your wallet. Some modern crypto debit cards even offer cashback.

Crypto Payment Processors: Compare Top Platforms for Businesses

How many blockchains support USDC?

A grand total of 33 blockchains support USDC, including each of the eight blockchains Slash users can utilize.

Post-Crypto Payment Management: Streamline Fiat Settlements with Slash

Read more from us