Accrual vs Deferral Accounting: Differences Explained

Timing is one of the most important elements of accounting and reconciliation. Services rendered, payments received, and bills incurred can land in very different parts of your financial statements depending on when cash changed hands and when the underlying activity actually occurred. Accruals and deferrals are the two mechanisms that ensure the timing of cash flow and the timing of economic reality stay in sync with each other on the books.

Both concepts live within accrual-basis accounting, the framework required under GAAP (Generally Accepted Accounting Principles) for most businesses and the standard that most lenders and investors expect financial statements to follow. The core idea of accrual accounting is that revenue and expenses should be recognized in the period they are earned or incurred, not in the period cash is received or paid. Accruals and deferrals are the adjusting entries that make this possible.

Getting these two concepts right can separate financial statements that accurately reflect the business from ones that paint a misleading picture of profitability. In this guide, we’ll explain accruals and deferrals in the context of accounting, then review key differences, examples, and potential mistakes. We’ll also take a look at Slash, a neobank that syncs two-ways with popular accounting platforms and comes with tools built to analyze your company’s current cash flow.¹

What Is an Accrual in Accounting?

An accrual is an accounting entry that recognizes revenue earned or an expense incurred before the corresponding cash transaction occurs. It records economic activity in the period it happens, regardless of when money moves.

The foundational principle behind accruals is the matching principle: expenses should be recognized in the same period as the revenue they help generate, and revenue should be recognized when it's earned, not when payment arrives. Without accruals, a business that delivers a month's worth of services in December but doesn't collect payment until January would show no revenue in December, even though the work was done.

Accruals come in two forms, one on each side of the income statement:

Accrued Revenue

Accrued revenue (also called unbilled revenue) arises when a business has earned revenue that it hasn't yet invoiced or received payment for. The service has been delivered, or the goods have been provided, but the cash hasn't arrived yet.

Example: A consulting firm completes a $15,000 engagement in December. The client will be invoiced in January and will pay in February. Under accrual accounting, the $15,000 is recognized as revenue in December (the period the work was done),not in January when the invoice goes out or February when cash arrives. The adjusting entry in December debits accounts receivable and credits revenue, recording both the asset and the income.

Until the cash is collected, accrued revenue appears on the balance sheet as a current asset, specifically as accounts receivable or accrued receivables. At that point, the asset converts to cash and the revenue was already recognized in the correct period.

Accrued Expenses

Accrued expenses are costs incurred in a period that haven't yet been paid or invoiced by the vendor. The business has received the service or goods, but the cash payment hasn't gone out yet.

Example: Employees work the last two weeks of December, but payroll for those two weeks doesn't process until January 3rd. The December financial statements should reflect the full month of wage expense, including those two weeks, even though no cash was paid in December. The adjusting entry debits “wages expense” and credits “wages payable”, recording the cost in the period it was incurred and the liability that will be settled in January.

Other common accrued expenses include interest payable (interest accumulating on a loan between payment dates), utilities incurred but not yet billed, and professional fees for services rendered but not yet invoiced. Each expense should be recorded in the period the economic activity occurred.

What Is a Deferral in Accounting?

A deferral is the opposite timing dynamic from an accrual. Where an accrual records an economic event before cash moves, a deferral records cash that has moved before the economic event has occurred. The cash came first, and the revenue or expense recognition comes later.

Deferrals also come in two forms:

Deferred Revenue

Deferred revenue (also called unearned revenue) arises when a business receives cash for goods or services it hasn't yet delivered. The cash is real and in the bank, but it can't be recognized as revenue yet because the business still owes something and the obligation hasn't been fulfilled.

Example: A SaaS company collects $12,000 for an annual software subscription on January 1st. The company has $12,000 in cash, but it has only earned one month of revenue by the end of January ($1,000). The remaining $11,000 is deferred revenue: a liability on the balance sheet representing the obligation to deliver 11 more months of service. Each month, $1,000 is recognized as revenue and the deferred revenue liability decreases by $1,000.

Deferred revenue is a liability, not income, until performance is complete. This is why software companies and subscription businesses often show large deferred revenue balances; they've collected cash that hasn't yet been "earned" under accounting standards.

Deferred Expenses (Prepaid Expenses)

Deferred expenses are costs paid in advance for benefits not yet received. When a business pays for something before consuming its value, the payment creates a prepaid asset that’s converted to an expense over time as the benefit is realized.

Example: A company pays $18,000 in January for a 12-month office lease running February through January. At the time of payment, none of this is an expense yet, since the business hasn't yet used any of the space. The payment creates a prepaid rent asset of $18,000. Each month, $1,500 is reclassified from the asset account to rent expense, matching the expense to the period the space is actually occupied.

Other common deferred expenses include prepaid insurance, prepaid software licenses, and annual subscription fees for tools or services that cover a period extending beyond the current month.

Key Differences Between Accruals and Deferrals

The essential distinction is the relationship between cash timing and recognition timing:

- Accruals: Revenue or expense is recognized before cash moves. The economic activity happened, but the cash hasn't caught up yet.

- Deferrals: Cash has moved before revenue or expense is recognized. The cash arrived early, but the economic activity hasn't caught up yet.

Accruals add entries that cash movement hasn't triggered yet, while deferrals delay the recognition of entries that cash movement has already triggered. Here’s a side-by-side comparison:

Practical Examples of Different Accounting Methods

Let’s look through a few concrete scenarios that demonstrate the differences between accruals and deferrals:

Annual insurance premium (deferral — deferred expense)

A business pays $6,000 in January for 12 months of business insurance. At payment, $6,000 is recorded as prepaid insurance (an asset). Each month, $500 is moved from prepaid insurance to insurance expense. By December, the full $6,000 has been expensed and the prepaid account is zero. If the full $6,000 were expensed in January, January's income statement would overstate costs by $5,500 and all subsequent months would understate them.

Interest on a loan (accrual — accrued expense)

A business has a $500,000 loan at 6% annual interest. Interest accrues daily, but the payment is due quarterly. The controller records accrued about $2,500 in interest expense at the end of each month, even though the payment hasn't been made yet. This ensures each monthly income statement reflects the true cost of carrying the debt, rather than showing a large interest expense only in the months when payments happen to fall.

Subscription revenue collected upfront (deferral — deferred revenue)

A B2B software company closes an annual contract on October 1st and collects $24,000 upfront. Over the four remaining months of the fiscal year, the company recognizes $2,000 per month as revenue. The remaining $16,000 (covering the following year's months) carries into the next fiscal year as deferred revenue, appearing as a liability on the balance sheet until the service is delivered. Recognizing the full $24,000 in October would overstate Q4 revenue and mask the company's actual performance in subsequent periods.

Project completed, invoice not yet sent (accrual — accrued revenue)

An engineering firm completes a project phase worth $40,000 in March but won't invoice until the final project report is delivered in April. The $40,000 is recognized as accrued revenue in March, appearing as a receivable on the March balance sheet. When the invoice is issued in April, the accrued receivable converts to a regular accounts receivable. This treatment ensures March's revenue reflects the work actually done in March.

Deferred rent (deferral — deferred expense)

A business signs a lease that includes a one-month rent-free period. Even though no cash is paid in month one, the total lease cost over the full term should be averaged across all months, creating a deferred rent liability that smooths the expense recognition over the lease period. This is especially relevant under ASC 842, the Financial Accounting Standards Board’s lease accounting standard that requires operating leases to be recognized on the balance sheet.

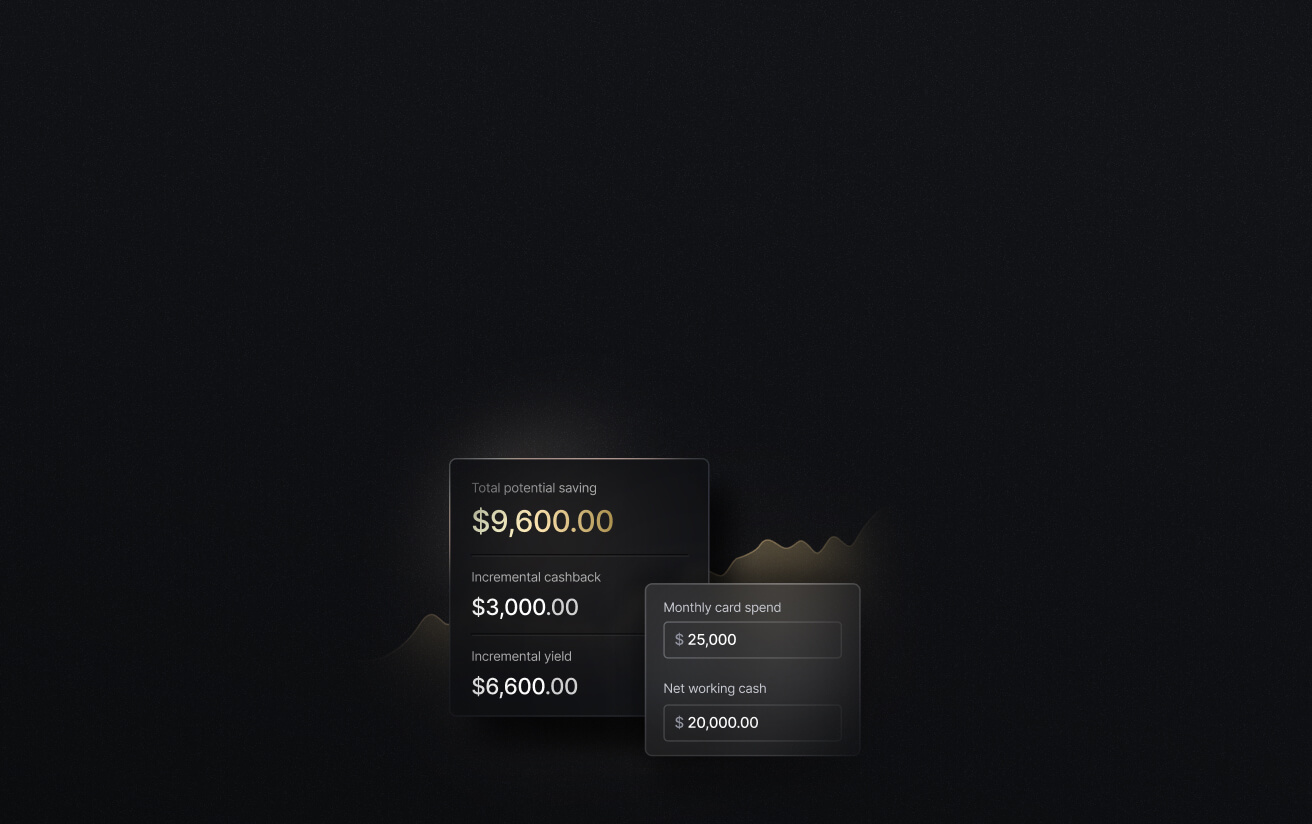

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

Why Accruals and Deferrals Matter for Business

Familiarizing yourself with both concepts and identifying them consistently is key for a few reasons, including:

- Accurate profit reporting: Without accruals and deferrals, income statements misstate the actual performance of the business in any given period. A consulting firm that bills quarterly might show huge profit in one month and near-zero profit in the next, even if the underlying work and value creation were steady throughout the quarter. Accruals smooth this into a truer picture of performance that can be useful for management decisions.

- Reliable balance sheets: Deferred revenue on the balance sheet tells lenders and investors that the business has cash obligations it hasn't yet fulfilled. Accrued liabilities tell them what's owed that hasn't yet been paid. Without these entries, the balance sheet understates obligations and overstates equity, often creating a misleading picture of financial strength for anyone evaluating the business from the outside.

- Tax and audit readiness: GAAP-compliant financial statements require appropriate accruals and deferrals. Businesses seeking outside financing, preparing for acquisition due diligence, or facing an audit should have clean, properly adjusted financials. Missing accruals or unrecognized deferrals are among the most common adjustments auditors make. Each one changes reported income and the financial ratios that matter to outside stakeholders, including debt covenants that may be tied to EBITDA or net income thresholds.

- Cash flow management: Understanding accruals and deferrals can help with cash flow planning, even though they're non-cash adjustments. A business with $500,000 in deferred revenue knows it has obligations to fulfill, while one with $300,000 in accrued expenses knows cash demands are coming. The accrual-basis financial statements, when read together with the cash flow statement, give the complete picture of both economic performance and actual liquidity.

Common Mistakes and How to Avoid Them

Even when you have their definitions down pat, it’s easy to make mistakes as you work with accruals and deferrals. Some of these errors might include:

- Missing period-end adjusting entries: One frequent error is simply overlooking the recording of accruals at period-end, thus letting the books reflect only cash transactions and deferring the adjustments to next month. This produces inaccurate monthly reports and makes the year-end close more complex.

- Letting deferred revenue balances go stale: Deferred revenue should be released as service is delivered. Businesses that collect annual fees but don't systematically release the liability each month accumulate deferred revenue balances that overstate obligations and understate current-period revenue.

- Confusing prepaid expenses with current-period costs: Paying for 12 months of a service in one transaction doesn't mean 12 months of expense hits in the current period. Properly deferring prepaid expenses protects margin accuracy in the payment month and ensures the expense is spread across the periods it benefits.

- Reversing accruals incorrectly: Many accrual entries are reversed in the following period when the actual invoice or payroll arrives. If reversals aren't set up correctly (or aren't done at all) the expense gets recorded twice, inflating costs in the period the actual transaction posts.

Keep Your Books Accurate Month-to-Month with Slash

When working with accruals and deferrals, your financial data should be current and accurate before the adjustment entries are made. Utilizing separate systems for banking, accounting, and employee spend can lead to missing expenses and receipts that turn end-of-month reconciliation into a mess. Slash was built to change that.

Slash is a business banking platform that keeps transaction data current throughout the month rather than collecting it at close. Every corporate card purchase is captured with receipt prompts at the moment of spend, categorized against the appropriate account, and sorted on our financial dashboard. Slash also integrates with QuickBooks Online, Sage Intacct, and Xero, meaning accounting data doesn’t have to be manually transcribed across systems. By the time the finance team sits down to record period-end accruals and release deferrals, the underlying transaction ledger is already accurate.

Our platform also allows users to make business purchases through a wide variety of payment rails, including card spend, global ACH, international wire transfers via SWIFT, real-time domestic payments through RTP and FedNow, and even stablecoins.⁴ No matter what method you use to make a purchase, all transactions are instantly recorded and visible on the Slash dashboard in real time.

Other helpful Slash features include:

- Reimbursements: Instead of managing reimbursements across multiple tools, teams can now submit, review, and approve reimbursements directly inside the Slash dashboard. Connect your bank account, upload your receipt, and let Slash capture the details.

- AI-powered finance: Our platform comes with Twin, a built-in AI agent that can be prompted with natural language to complete complex tasks. Users can ask it to create cards, pay invoices, review your cash flow, and much more.

- Slash Visa® Platinum Card: The Slash Card allows you to set customizable spending controls and issue unlimited virtual cards for handling team expenses, vendor payments, subscriptions, and more. Users can also earn up to 2% cash back on business purchases.

- Working capital financing: Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to help bridge cash flow gaps.⁵

- High-yield treasury: Earn up to 3.80% annualized yield on idle funds with money market investments from BlackRock and Morgan Stanley, managed directly within your Slash account.⁶

Check out Slash today if you’re looking to keep your financial data clean, centralized, and accurate.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

Frequently asked questions

What is GAAP (Generally Accepted Accounting Principles)?

GAAP is the set of standardized rules, conventions, and procedures used in the United States for financial reporting. They ensure consistency, accuracy, and comparability in financial statements for public companies, non-profits, and governments, and they’re primarily managed by the FASB.

Year-End Accounting Checklist: 12 Steps for Success

What is accrual accounting?

Accrual accounting is simply an accounting method that mainly centers around accruals. It records revenue when earned and expenses when incurred, rather than when cash actually changes hands.

Are wages paid through accrual or deferral accounting?

Wages are primarily paid and recorded through accrual accounting. Under this method, salary and wage expenses are recognized in the period work is performed, even if the cash payment occurs later.

What is Payroll Processing? Steps, Challenges, and Solutions

Read more from us