What is Vertical-Specific Banking and Why it Matters for Your Business

Managing your business’s finances can sometimes feel like forcing a square peg into a round hole. Most traditional banks treat every business the same: you get a checking account, a credit card, and access to a generic portal that wasn't built with your industry in mind. But what if your financial provider actually understood your business? What if banking could be customizable, automated, and unified around the products and services you actually need?

That's the vertical-specific approach, and it's what defines Slash. Vertical banking means designing financial products around the nuanced needs of a particular industry or customer segment, rather than offering one-size-fits-all solutions.¹ At Slash, we provide tailored solutions for ecommerce operators, affiliate marketers, healthcare suppliers, ticketing companies, travel agencies, and more.

In this guide, we introduce vertical-specific banking and explore how it applies across industries, what to evaluate when comparing platforms, and how integrations, partner models, and embedded finance shape the experience. We also outline the practical advantages of working with a vertical-specific provider such as Slash, a financial platform designed to adapt to your business model rather than requiring you to adjust your operations to a generic bank.

Key benefits of vertical-specific banking solutions

Vertical-specific banking offers a more tailored approach to managing your company’s finances.

A general-purpose bank is like a family doctor: capable across a wide range of needs but not specialized. A vertical-specific banking solution is more like a specialist, focused on a specific industry with expertise and tools that a generalist cannot match.

In practice, that means your financial provider understands the cash flow patterns, revenue cycles, regulatory landscape, and unique risks of your industry. A financial provider focused on wine and spirits knows that wineries carry long inventory cycles and seasonal revenue. One serving law firms understands trust accounts and contingency fee structures. One built for cannabis companies knows how to navigate a complex compliance environment.

Slash is a vertical-specific banking platform designed for select industries, including marketing agencies, travel agencies, healthcare suppliers, ecommerce businesses, Web3 companies, foreign SMBs, contractors, and others.¹ Below are some of the advantages of working with a financial provider tailored to your industry:

- Support that understands your industry: Slash's support team is available 24/7 to help with any issues or financial management questions. We have industry awareness across crypto-based businesses, ecommerce sellers, marketing agencies, wholesalers, healthcare companies, and more.

- Underwriting that fits your business model: The spending power of the Slash Card scales with your business's current financial position. Rather than relying on a credit check, we assess your current financials to determine eligibility. You can also access working capital through our tailored line of credit, provided in partnership with Slope.⁵

- Rewards built around how your business spends: The Slash card earns up to 2% cash back, a flat-rate model that rewards diverse spending categories at an industry-leading rate. Slash Perks add millions of dollars in exclusive discounts and credits for tools like HubSpot, Google Cloud, QuickBooks, Intercom, and more.

- Configurability across products and services: Slash adapts to your business based on your scale, location, and team size. International businesses can use Slash’s Global USD account to access U.S. dollar banking without a U.S.-registered LLC or bank account.³ Larger enterprises can use the dashboard to issue unlimited virtual cards, manage AP and AR, automate approvals, and maintain centralized visibility and control across teams.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

Essential criteria for selecting a vertical banking platform

Since vertical-specific financial platforms tailor their services to a defined set of industries, it's worth taking the time to find the right fit rather than signing up for the first option you come across. The benefits of vertical banking are real, but only if you choose a provider that actually aligns with your business needs. Here are the key considerations to keep in mind:

Industry fit

The first and most obvious question is whether the provider actually serves your industry. A clear sign: look for a dedicated section on their website that explains specifically how their products and services apply to businesses like yours. If you're drawn to a platform but aren't sure how it maps to your needs, reach out to their sales team before committing. The quality of that conversation (how well they understand your business without you having to explain the basics) will tell you a lot.

Compliance, risk, and security measures

Not every financial services provider will meet your compliance and security requirements, and the stakes vary significantly by industry. At Slash, for example, we maintain SOC II Type 2 certification, which allows us to serve businesses in the healthcare sector while meeting the strict data security and protection standards required by HIPAA. If your business operates in a regulated or risk-sensitive segment, carefully review a provider's compliance certifications, security infrastructure, and terms of service before signing on.

API capabilities

One major advantage modern fintech platforms have over traditional banks is API configurability. Application programming interfaces, or APIs, allow your banking platform to connect directly with the other tools in your tech stack, including your ERP, accounting software, and payment processors. This enables automated workflows, real-time data synchronization, and reduced manual reconciliation. Slash’s API allows you to programmatically create and manage accounts, issue and control virtual cards, initiate payments, and embed financial functionality directly into your existing systems.

AI and advanced analytics features

Vertical-specific banking has been made possible in large part by artificial intelligence. AI enables platforms to learn your spending patterns over time, flag suspicious activity with greater accuracy than rule-based systems, and surface insights that help you make smarter financial decisions. For businesses with high transaction volume or complex revenue streams, advanced analytics can also provide real-time visibility into cash flow, category-level spending, and forecasting.

Pricing structures

Before vertical-specific banking, many specialized financial services were limited to enterprise providers charging tens of thousands of dollars per year. Platforms like Slash have changed that by offering a wide range of industry-specific features at no cost, including crypto-native financial management, integrated treasury tools, tailored financing, and advanced analytics.⁴, ⁶ When evaluating a provider, review what is included in the base plan versus premium tiers, and ensure the pricing model scales reasonably as your business grows.

Step-by-step process to choose and onboard a vertical fintech bank

Switching financial providers or setting up business banking for the first time can be daunting. But with the right process, it can be fairly straightforward. Here's how to approach it:

Step 1: Evaluate your current financial setup

Before you start evaluating providers, take stock of what you have and what's missing. What tools do you use today for payments, expense management, and accounting? Where are the friction points? What does your current provider not support that you wish it did? This baseline will help you evaluate new options with a clear picture of what you actually need.

Step 2: Define your non-negotiables

Identify the criteria that matter most, whether that's industry-specific compliance, API connectivity with your existing software, credit availability, or international payment support. Consider ranking them in order of importance so you can make a clear decision if no single provider checks every box.

Step 3: Create a shortlist of providers with good industry fit

Research different providers, and use the criteria outlined in the previous sections to narrow down your list of options. Prioritize platforms that explicitly serve your industry, not ones that simply don't exclude it. Read case studies, look for customer reviews from businesses in your sector, and pay attention to how specifically they speak to your industry's challenges.

Step 4: Reach out to the sales team with questions

Schedule demos with your shortlisted providers and come prepared. Ask how they handle compliance requirements specific to your industry, what their API documentation looks like, how underwriting decisions are made, and what happens if your business grows or your needs change. How fluently they answer will tell you whether their vertical expertise is real or surface-level.

Step 5: Run a parallel pilot if possible

Rather than switching cold, consider running your new platform in parallel with your existing setup for a short period. This gives you a chance to stress-test the product with real transactions, evaluate support responsiveness, and identify integration issues before you've fully committed.

Step 6: Migrate and integrate

Once you're ready to make the switch, update your payment details with vendors and customers, connect your third-party software, and set up your card and spend controls. Most modern fintech platforms have onboarding support to walk you through this; take advantage of it.

Core product categories in vertical banking

Understanding what vertical banking platforms actually offer, and how those products differ from what traditional banks provide, can help you evaluate your options more clearly to make sure you're getting full value from the platform you choose. Here are some of the standard features offered by modern financial platforms and how a vertical-specific approach changes their functionality:

Payments and money movement

Every business needs to send and receive money reliably. Vertical banking platforms like Slash support domestic and international wires, ACH, and real-time payment rails. Where Slash stands out is in configuring these capabilities for specific industries. An ecommerce business may benefit from integrations with Stripe or Shopify, while a healthcare supplier may require specialized billing and reimbursement workflows. Look for platforms that offer fast settlement, transparent foreign exchange rates, and automation for recurring payments or disbursements.

Lending and financing options

Access to capital is one of the most impactful ways a vertical banking platform can support your business. Unlike traditional banks, which rely primarily on credit scores and historical financials, many fintech lenders use alternative underwriting models that evaluate real-time revenue, transaction data, and industry-specific metrics. Slash Capital offers a tailored line of credit that allows flexible drawdowns with 30-, 60-, or 90-day repayment terms to help manage short-term liquidity needs.

Corporate cards and spend management

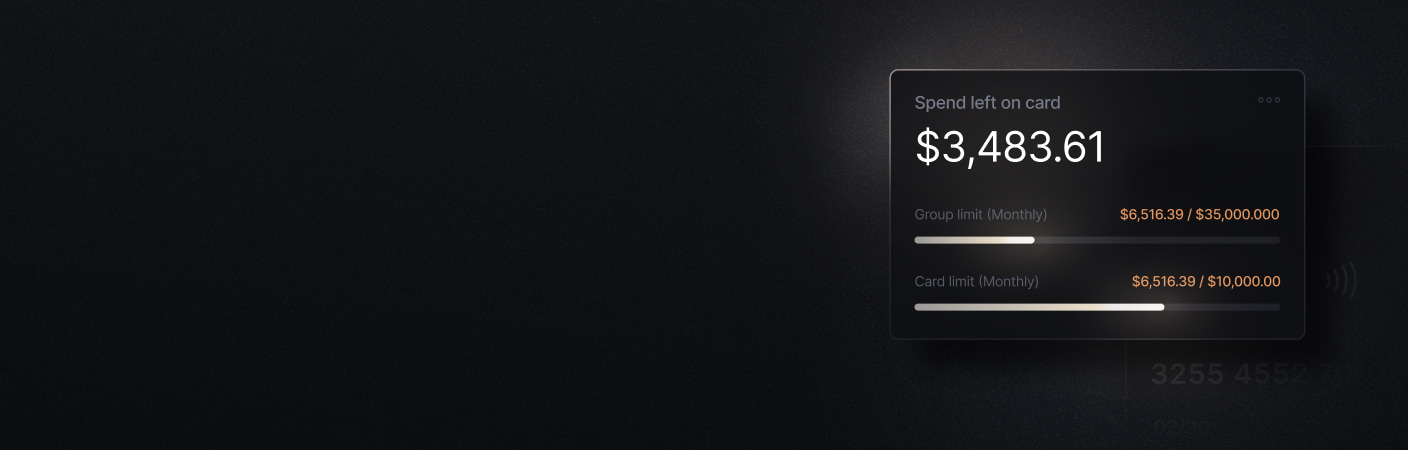

Modern spend management tools allow you to issue unlimited virtual cards, set granular spending limits by employee or department, and monitor transactions in real time. For teams with high transaction volume, this level of control reduces unauthorized spend, simplifies expense reporting, and minimizes reconciliation work. With the Slash card, you get these features along with cashback of up to 2%.

Bank accounts and treasury services

Beyond standard checking and savings functionality, Slash offers treasury management tools that help you optimize how idle cash is deployed, earn yield on operating balances, and maintain visibility across multiple accounts or entities from a single dashboard. For businesses operating internationally, the Slash Global USD account, which allows foreign businesses to hold and transact in U.S. dollars without needing a U.S.-registered entity, can remove significant friction from cross-border operations.

Integrations and partner models in vertical banking

Vertical banking is powered by a combination of regulated institutions and technology partners working together behind the scenes. These integrations determine how accounts are structured, how funds move, and how financial tools are delivered within software platforms. To assess any vertical banking provider, it is important to understand the partner models that support it:

Banking-as-a-service and whitelabel solutions

Banking-as-a-service (BaaS) is the infrastructure layer that powers most modern fintech platforms. Instead of obtaining their own banking charter, fintech companies partner with licensed banks to access core capabilities such as deposit accounts, card issuance, and payment processing.

White-label solutions extend this model by enabling businesses to offer branded financial products to their own customers without building the underlying infrastructure. For example, a software platform serving independent restaurants might embed a branded business account or payment card within its product, powered by a BaaS provider behind the scenes.

Partner banks and payment facilitators

Behind every fintech platform is a network of institutional partners that enables it to operate. Partner banks, often referred to as sponsor banks, are FDIC-member institutions that provide the regulated banking infrastructure on which fintech platforms rely.

Slash partners with Column N.A. to offer FDIC-insured bank accounts and charge cards.² Client funds are supported by FDIC insurance through Column’s insured cash sweep network, which allocates deposits across multiple institutions to provide coverage beyond the standard $250,000 limit.

Embedded financial technology

Embedded finance integrates financial functionality directly into the platforms where businesses already operate, whether that is accounting software, an ERP system, an ecommerce dashboard, or industry-specific management tools. For example, if a healthcare supplier can approve a purchase order and access working capital from the same interface used to manage inventory, that is embedded finance in practice.

Look for platforms with strong integrations across the tools common in your industry, clear API documentation, and a partner ecosystem that reflects a practical understanding of how your business operates.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

How Slash can drive business growth with vertical-specific solutions

Slash is built around the operational realities of modern businesses, not legacy banking assumptions. Instead of offering a generic account and leaving you to piece together the rest, it integrates payments, capital access, and spend controls into a system that reflects how your revenue flows, how your team operates, and how your industry is regulated.

When your financial tools match your business model, decisions can move faster, cash flow can be easier to manage, and fewer resources are spent navigating limitations or workarounds. Instead of reshaping your operations to fit a bank’s constraints, you work with infrastructure that adjusts to the way you already run your business.

Here’s what you get with Slash:

- Slash Visa® Platinum Card: Earn up to 2% cash back on business expenses, set customizable spending controls and limits, and issue unlimited virtual cards for your team members, vendor payments, and subscriptions.

- Accounting integrations: Automatically sync transaction data with QuickBooks for simplified reconciliation and reporting. Use Plaid to connect with additional financial tools, or import data from Xero to enhance your accounting workflow.

- Diverse payment methods: Support for global ACH settlement, wire transfers to 180+ countries, and real-time payment rails like RTP and FedNow. Pro users pay no additional per-transaction fees.

- Working Capital Financing: Access short-term financing with flexible 30-, 60-, or 90-day repayment terms to bridge cash flow gaps when needed.

- High-yield treasury accounts: Earn up to 3.86% annualized yield on idle funds with money market investments from BlackRock and Morgan Stanley, all managed directly from your Slash account.

Apply in less than 10 minutes today

Join the 3,000+ businesses already using Slash.

Frequently asked questions

What distinguishes vertical fintech banking from traditional banking?

Vertical fintech banking is designed around the needs of specific industries rather than serving all customers with a standardized product set. It combines financial infrastructure with industry-specific workflows, integrations, and underwriting models that traditional banks typically do not provide.

What are the key security and compliance checks to consider?

Evaluate whether the platform partners with regulated, FDIC-member banks and follows established compliance standards such as KYC, AML, and sanctions screening. You should also review how funds are safeguarded, how data is protected, and whether the provider maintains clear audit and reporting processes.

How important are APIs and integrations for vertical fintech solutions?

APIs and integrations allow financial services to connect directly with your accounting software and other operational tools. API integrations can reduce manual reconciliation, enable automation, and ensure financial data flows seamlessly across your systems.